From Weavers to Bankers in Two Generations

Hans Fugger arrived in Augsburg in 1367 with nothing but the skills of a country weaver from the village of Graben. He was, by the standards of his time, nobody. Augsburg was already a prosperous imperial free city, its wealth built on the textile trade that connected the workshops of southern Germany to the markets of Venice and the wider Mediterranean. Hans married well, accumulated modest capital through the linen trade, and died in 1408 as a respected but unremarkable citizen. His sons expanded the business, trading in spices, silk, and cloth alongside the original linen operations. By the mid-fifteenth century, the Fugger family had become one of several successful merchant houses in Augsburg. Comfortable. Not extraordinary.

Then came Jakob.

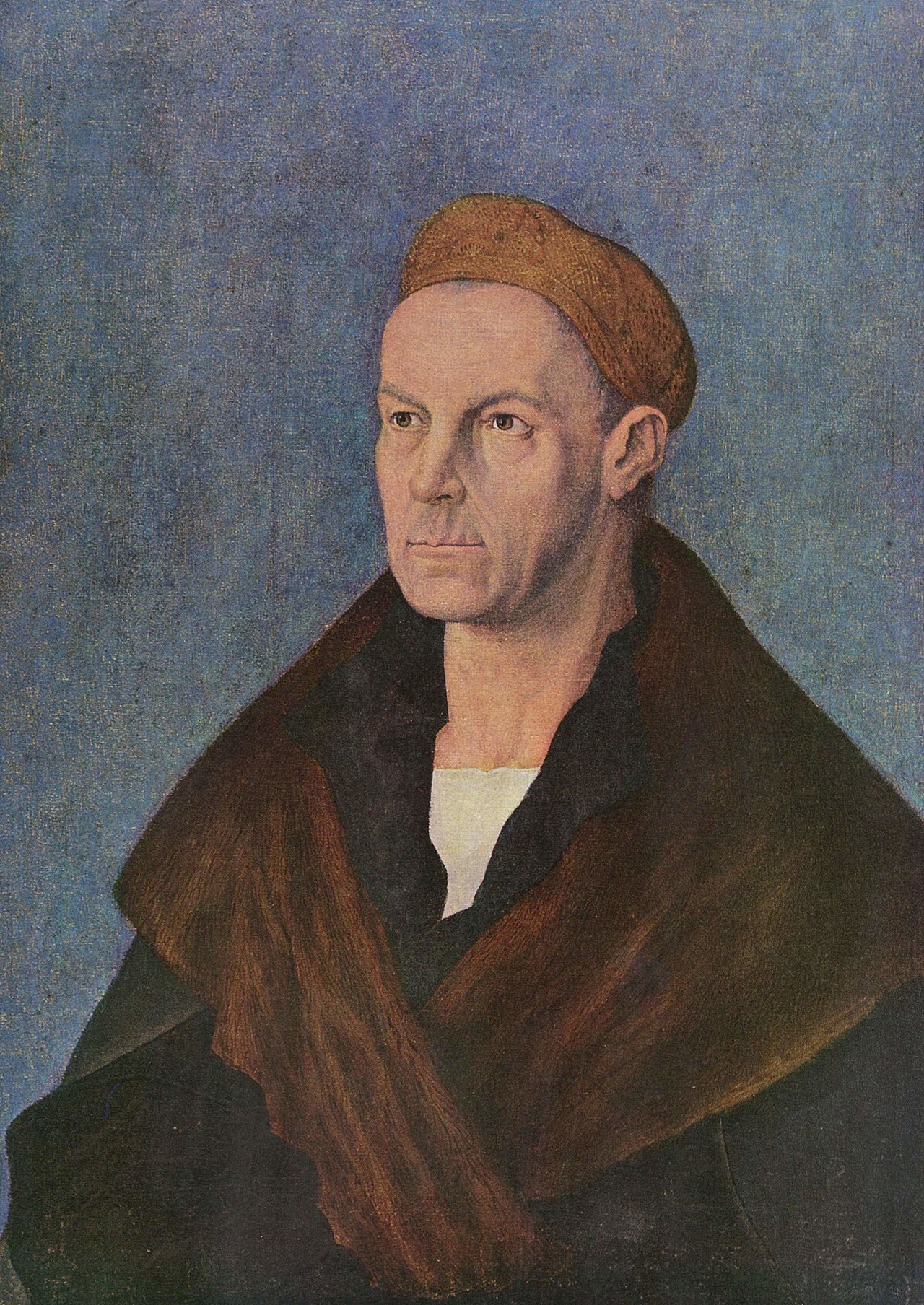

Born in 1459 as the tenth of eleven children, Jakob Fugger was originally destined for the Church. His older brothers already ran the family trading firm, and the youngest son seemed surplus to commercial requirements. But when his brother Markus died in 1478, Jakob was recalled from his ecclesiastical studies and redirected toward business. He was sent to Venice, the commercial capital of the known world, to learn the trade. It was a decision that would reshape European finance (Steinmetz, 2015).

The Venetian Education

Venice in the 1470s was the most sophisticated commercial center on earth. Its merchants had pioneered maritime insurance, double-entry bookkeeping, and complex partnership structures centuries before the rest of Europe caught up. The Fondaco dei Tedeschi, the German trading house on the Grand Canal where northern merchants conducted their business, was Jakob's school. Here he learned not merely how to buy and sell goods, but how to think about money itself as a commodity to be deployed, leveraged, and multiplied.

What distinguished Jakob from his fellow apprentices was an unusual capacity for systematic thinking. He did not merely learn the mechanics of double-entry bookkeeping; he grasped its deeper implications. If every transaction could be recorded as both a debit and a credit, then the entire financial position of an enterprise could be rendered visible at a glance. Cash flows, outstanding debts, inventory values, profit margins — all could be tracked with a precision that most merchants of the era would have found bewildering. Jakob returned to Augsburg in the early 1480s with a set of analytical tools that his competitors simply did not possess (Haberlein, 2012).

He also returned with something equally valuable: connections. The Venetian trading networks extended from Constantinople to London, from Lisbon to the spice ports of the Levant. Jakob had learned how these networks operated, who controlled them, and where the greatest profits lay. Crucially, he had observed how the Venetian state itself functioned as a borrower, issuing bonds through the Monte Vecchio and paying interest from tax revenues. Sovereign debt, he understood, was not merely a financial instrument. It was a mechanism of power.

The Copper King

Jakob Fugger's path to unimaginable wealth began not in a counting house but in a mine shaft. In the 1480s, he recognized an opportunity that no other Augsburg merchant had fully exploited: the rich silver and copper deposits of the Habsburg lands in Tyrol and Hungary. Mining was an expensive, technically demanding enterprise. Individual mine operators lacked the capital to invest in drainage systems, ventilation shafts, and smelting furnaces. They needed credit. Jakob was willing to provide it — at a price.

His method was elegantly simple and ruthlessly effective. He advanced loans to mine operators secured against their future output. When the operators inevitably struggled to repay, Jakob foreclosed and acquired direct ownership of the mines themselves. By the 1490s, he had assembled what amounted to a vertical monopoly: he owned the mines, controlled the smelting operations, and managed the trading networks that distributed copper and silver across Europe. No competitor could match this level of integration (Ehrenberg, 1928).

The scale was staggering. Hungarian copper, mined primarily in Neusohl (modern Banska Bystrica in Slovakia), accounted for roughly half of total European copper production. Tyrolean silver from the mines around Schwaz was equally critical, providing the raw material for coinage across the Holy Roman Empire. Jakob Fugger controlled both.

| Commodity | Primary Source | Fugger Control | European Market Share |

|---|---|---|---|

| Copper | Neusohl, Hungary | Direct ownership of mines and smelters | ~50% of European production |

| Silver | Schwaz, Tyrol | Mining leases secured by Habsburg loans | ~40% of Central European production |

| Mercury | Almaden, Spain | Lease from Spanish crown | Near-monopoly |

| Textiles | Augsburg workshops | Family's original trade | Significant regional presence |

This was not banking in the Medici sense of letters of credit and foreign exchange. It was industrial capitalism avant la lettre — the integration of resource extraction, manufacturing, and distribution under a single controlling entity. When competitors or governments complained about Fugger's monopolistic practices, he responded with the cold logic of a man who understood that control of supply conferred control of price. In 1523, when the Reichstag debated a proposal to break up monopolies, Jakob used a combination of political pressure and legal argument to ensure the legislation died quietly.

Banker to the Habsburgs

Mining made Jakob Fugger rich. Sovereign lending made him powerful. The relationship between the Fugger bank and the Habsburg dynasty was symbiotic in the most literal sense: each needed the other to survive.

Emperor Maximilian I, who ruled the Holy Roman Empire from 1493 to 1519, was perpetually at war and perpetually short of cash. His military campaigns against France, Venice, and the Ottoman Empire consumed revenues faster than his sprawling but inefficient tax system could generate them. Maximilian needed a banker who could advance large sums quickly and reliably, without the delays inherent in calling an imperial diet and negotiating tax levies with dozens of recalcitrant princes. Jakob Fugger was that banker.

The arrangement worked because it was secured by something more tangible than a sovereign's promise to repay. Fugger loans to Maximilian were collateralized by mining revenues, toll receipts, and the output of specific Habsburg territories. When Maximilian borrowed 170,000 florins to finance his war in Italy, he pledged the silver output of the Tyrolean mines as security. If the emperor defaulted, Fugger simply kept mining — and selling — the silver. This collateral structure insulated Fugger from the catastrophic risk that had destroyed earlier banking dynasties. The Bardi and Peruzzi of Florence had been ruined in the 1340s when Edward III of England defaulted on their loans with nothing but royal gratitude offered as security. Jakob Fugger was not interested in gratitude.

Between 1490 and 1525, the Fugger fortune grew from approximately 54,000 guilders to over 2 million — a nearly fortyfold increase in a single generation. No other private fortune in European history had grown at anything like this rate. For comparison, the entire Medici Bank at its peak under Cosimo held assets of roughly 290,000 florins. Jakob Fugger's personal wealth dwarfed the greatest banking house of the previous century.

Buying an Emperor

The supreme demonstration of Fugger's financial power came in 1519, when the electors of the Holy Roman Empire gathered to choose a successor to the recently deceased Maximilian I. Imperial elections were, in practice, auctions. Each of the seven electors expected substantial payments in exchange for their votes, and the two leading candidates — Charles of Spain (Maximilian's grandson) and Francis I of France — competed to offer the most lavish inducements.

Jakob Fugger organized the financing that secured the throne for Charles. The total cost of the election was approximately 852,000 florins, of which Fugger personally contributed 543,585 florins — nearly two-thirds. The Welser banking family of Augsburg contributed an additional 143,000 florins, and Italian bankers provided the remainder. The money was distributed to the electors through an ingenious mechanism: Fugger deposited funds with agents in each electoral city, to be released only upon confirmation that the elector had voted for Charles. It was, in effect, an escrow arrangement — payment contingent on performance (Steinmetz, 2015).

Charles won. He became Charles V, Holy Roman Emperor, King of Spain, ruler of the Netherlands, and sovereign of the vast Spanish possessions in the Americas. He was, on paper, the most powerful monarch in Europe. And he owed his throne to a merchant from Augsburg.

Jakob Fugger was not shy about reminding him. In a letter that has become one of the most quoted documents in financial history, Fugger wrote to Charles in 1523, demanding repayment of overdue loans. The key passage — remarkable for its directness in an age of elaborate courtly deference — read: "It is well known that Your Imperial Majesty could not have acquired the Imperial Crown without my help." No banker before or since has addressed a reigning emperor with such blunt assertion of financial leverage. The letter worked. Charles arranged partial repayment.

The Papal Connection and the Spark of Reformation

Fugger's reach extended beyond secular politics into the very heart of the Catholic Church. His agents operated across Europe as collectors of papal revenues, handling the transfer of funds from distant dioceses to Rome with an efficiency that the Church's own administrative apparatus could not match. This role generated steady commission income, but its most consequential dimension was its entanglement with the sale of indulgences — a practice that would help ignite the Protestant Reformation.

In 1514, Albrecht of Brandenburg sought appointment as Archbishop of Mainz, one of the most prestigious ecclesiastical positions in the Holy Roman Empire. The appointment required a substantial payment to Rome — a fee known as the pallium — and Albrecht, already archbishop of Magdeburg, needed a special papal dispensation to hold multiple sees simultaneously. The total cost was approximately 29,000 ducats. Albrecht did not have the money. Jakob Fugger lent it to him.

The repayment mechanism was audacious. Pope Leo X authorized Albrecht to sell indulgences — certificates offering remission of punishment for sins — throughout his territories, with half the proceeds going to Rome to finance the construction of St. Peter's Basilica and half going to repay Albrecht's debt to the Fuggers. The Dominican friar Johann Tetzel was dispatched to sell these indulgences with a fervor that became legendary. His methods — including the reported slogan that a coin dropped in the collection box would release a soul from purgatory — scandalized reformers across Germany (Haberlein, 2012).

On October 31, 1517, Martin Luther nailed his Ninety-Five Theses to the door of the Castle Church in Wittenberg. Among his central grievances was the sale of indulgences, which he attacked as theological corruption and financial exploitation. Luther was well aware of the Fugger connection. He denounced the arrangement by which papal revenues flowed through Fugger counting houses, and in his 1520 tract "An Address to the Christian Nobility of the German Nation," he called explicitly for action against monopolists, with the Fuggers as his primary target.

Jakob Fugger had not intended to trigger a religious revolution. He had simply arranged a profitable loan. But the transaction revealed how deeply financial networks had penetrated the institutional structures of the Church, and how the pursuit of profit could generate consequences far beyond the counting house.

The Fuggerei: A Legacy in Stone

In the same year that Luther's challenge to papal authority was escalating into open schism, Jakob Fugger undertook a project of an entirely different character. In 1521, he established the Fuggerei, a housing complex in Augsburg designed to provide shelter for the city's impoverished Catholic citizens. The complex comprised 52 houses containing 106 apartments, surrounded by walls and gates that were locked each night.

The terms of residence were remarkable. Annual rent was set at one Rhine guilder — a purely nominal sum even by sixteenth-century standards. Residents were required to be Catholic citizens of Augsburg who had fallen into poverty through no fault of their own, and they were obligated to pray three times daily for the souls of the Fugger family. The foundation was endowed with sufficient capital to sustain itself in perpetuity.

Five centuries later, the Fuggerei still operates under essentially the same terms. The annual rent remains one Rhine guilder, now equivalent to 0.88 euros. Residents still pray for the Fuggers. The complex was heavily damaged during World War II but was rebuilt and expanded. It is the oldest social housing project in the world still in continuous operation — a tangible monument to a man whose other legacies are recorded in ledgers and diplomatic archives. Among its residents was the great-grandfather of Wolfgang Amadeus Mozart, a Fugger bricklayer named Franz Mozart who lived there in the late seventeenth century.

Fugger Versus Medici: Two Models of Banking Power

Comparing the Fugger and Medici banking empires illuminates two fundamentally different approaches to the accumulation of financial power. The Medici model was horizontal: a network of urban branches connected by correspondent banking relationships, generating profit from trade finance, foreign exchange, and the management of papal revenues. The Fugger model was vertical: direct control of commodity extraction integrated with sovereign lending, where loans to rulers were secured by the very mines and toll stations that generated the underlying wealth.

Each model carried characteristic risks. The Medici were vulnerable to agency problems in their far-flung branch network — disloyal managers, unauthorized lending, and the slow erosion of oversight that distance inevitably produced. Their decline was driven by the failure of branch managers to exercise discipline and by the diversion of bank resources to political purposes under Lorenzo the Magnificent.

The Fugger risk was different: concentration. By tying their fortune so tightly to the Habsburgs, the Fuggers created a dependency that neither party could easily escape. When Habsburg finances deteriorated, the Fuggers had no choice but to extend additional credit to protect their existing claims — a dynamic that modern bankers would recognize as throwing good money after bad. The Rothschild dynasty of the nineteenth century would avoid this trap by diversifying across five national markets, ensuring that no single sovereign default could threaten the family's survival.

Death and the Inheritance of Risk

Jakob Fugger died on December 30, 1525, at the age of sixty-six. He had never married until late in life, wedding Sibylle Artzt in 1498, and had no surviving children. Control of the firm passed to his nephew Anton Fugger, who at thirty-two inherited the largest commercial enterprise in Europe.

Anton was a capable manager who initially expanded the family's operations further. Under his stewardship, the firm's total assets grew from approximately 2.1 million guilders at Jakob's death to over 5 million guilders by the mid-1540s. He maintained the firm's position as primary banker to Charles V, financing the emperor's wars against France, the Ottoman Empire, and the Protestant princes of Germany.

But the structural vulnerabilities that Jakob had managed through sheer force of personality and political acumen became increasingly apparent under Anton. Charles V abdicated in 1556, dividing his empire between his son Philip II (who received Spain and the Netherlands) and his brother Ferdinand I (who received the Habsburg lands in Central Europe and the imperial title). The Fuggers now had to manage relationships with two sovereign borrowers instead of one, each of whom was financially overextended.

The Spanish Bankruptcies and the Long Decline

Philip II of Spain, inheritor of an empire on which the sun famously never set, was also the inheritor of debts that exceeded his revenues by a widening margin. In 1557, he declared a suspension of payments — effectively a sovereign default — on his obligations to his bankers. The Fuggers, as his largest creditors, bore the heaviest losses.

The default was restructured rather than repudiated outright. Philip converted his short-term debts into long-term bonds (juros) bearing lower interest rates, and the Fuggers accepted the terms because the alternative — total loss — was worse. But the pattern repeated. Philip declared bankruptcy again in 1575, and yet again in 1596. Each default eroded the Fugger fortune further.

Anton Fugger died in 1560, and subsequent generations lacked both the appetite and the ability to sustain the firm's banking operations at their former scale. The family gradually withdrew from active commerce and finance, investing instead in the acquisition of landed estates, lordships, and noble titles. By the early seventeenth century, the Fuggers had transformed themselves from merchants and bankers into landed aristocrats — a common trajectory for successful commercial families in early modern Europe, but one that represented a fundamental retreat from the source of their original power.

The Fugger Newsletters: Pioneers of Financial Intelligence

One dimension of the Fugger legacy deserves particular attention: the family's role as pioneers of organized financial information. From the 1560s onward, the Fugger network maintained a systematic correspondence service — the Fuggerzeitungen, or Fugger newsletters — that collected and distributed commercial, political, and military intelligence from across Europe and beyond. Correspondents in major cities compiled reports on commodity prices, shipping movements, political developments, military campaigns, and diplomatic negotiations, forwarding them to the Fugger headquarters in Augsburg for consolidation and redistribution.

Approximately 16,000 of these handwritten newsletters survive in the Austrian National Library in Vienna, covering the period from 1568 to 1605. They represent one of the earliest systematic attempts to organize economic and political information for commercial purposes — a precursor to the financial news services that would emerge centuries later with Reuters and Bloomberg. The newsletters gave the Fuggers and their correspondents an informational advantage that was, in its own way, as valuable as their mining monopolies. In markets where information traveled at the speed of a horse, knowing a fact days or weeks before your competitors was worth a fortune.

Legacy: The Price of Lending to Sovereigns

Jakob Fugger's career poses a question that has echoed through every subsequent century of financial history: what happens when private capital becomes so intertwined with sovereign power that the two can no longer be separated? Fugger financed emperors, purchased papal appointments, and controlled the mineral wealth of half a continent. In return, he received monopoly concessions, mining rights, and political protection that no purely market-based competitor could overcome. The arrangement generated extraordinary wealth — but it also created a dependency that proved fatal once the sovereign borrower's credit deteriorated.

The pattern recurred with remarkable consistency. The Genoese bankers who replaced the Fuggers as Spain's primary creditors in the late sixteenth century suffered the same fate when Philip III defaulted in 1607. The great Amsterdam banking houses of the eighteenth century were weakened by their exposure to sovereign debt during the French Revolutionary Wars. Even the Rothschilds, for all their sophistication and diversification, discovered during the revolutions of 1848 that sovereign lending carried political risks that no amount of financial engineering could fully eliminate.

Jakob Fugger understood this dynamic better than most. His famous letter to Charles V was not merely an exercise in impertinence; it was a creditor's assertion that the debtor-creditor relationship, even when the debtor wore an imperial crown, imposed obligations that could not be evaded. The emperor needed the banker as much as the banker needed the emperor. In that mutual dependency lay both the source of Fugger's extraordinary power and the ultimate cause of his dynasty's decline — for when the balance shifted and the sovereign decided that default was preferable to repayment, no letter, however boldly worded, could compel a king to honor his debts.

The Fuggerei still stands in Augsburg, its gates locked each night at ten, its rent unchanged in five centuries, its residents still murmuring prayers for a family whose counting houses once held the finances of half of Europe in their ledgers.

Related

Historical records Learn more about our methodology.