The Continental Currency: Not Worth a Continental (1775-1783)

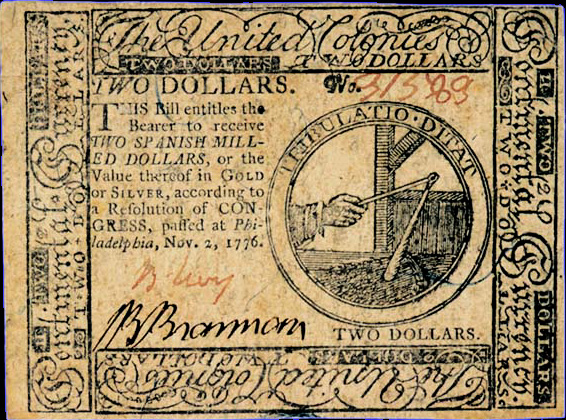

On 22 June 1775, five days after Bunker Hill, the Second Continental Congress sat in the Pennsylvania State House on Chestnut Street and voted to emit two million Spanish milled dollars' worth of paper bills. There was no treasury. There was no tax base. There was not even a formal confederation — the Articles would not be ratified for another six years. What Congress did have was a printer on Market Street named Hall and Sellers, willing to run copperplate on thick rag paper, and a war that had to be paid for on Monday morning. The resolution that authorised the first emission took up a single paragraph in the minutes and made the thirteen colonies collectively liable for redemption "in Spanish milled dollars, or the value thereof in gold or silver," at a future date to be determined. That future date never arrived.

Paper bills came off the press in August. They were printed in denominations from one-sixth of a dollar up to eighty dollars, with Latin mottoes and elaborate nature designs cut by Benjamin Franklin's printer friends — a mulberry leaf, a cluster of grapes, a sheaf of wheat — specifically chosen because engraving them was difficult and counterfeiters would, in theory, be slow. On the back, a line of the original copper printing: "The United Colonies." By the time the Declaration of Independence was signed, the paper was circulating from New Hampshire to Georgia, redeemable in theory by state quotas that Congress set but could not enforce. The system worked, at first, because a war fever willed it to. For a few months, a Continental dollar bought a Continental dollar of goods.

A Congress that could not tax

To understand the currency, start with the constitutional hole under it. The Second Continental Congress was an ad hoc body of state delegates with no power to levy taxes, no power to compel the states to send money, and no sovereign credit standing with European bankers. Its one reliable instrument was the printing press. Congress issued bills of credit forty times between June 1775 and November 1779, producing an aggregate face value of roughly $241.6 million according to the detailed ledger reconstructed in (Ferguson, 1961). The individual states, running their own war administrations, printed a further $209.5 million in state-chartered currencies. Together, more than $450 million of paper face value was laid on a colonial economy whose hard-coin stock in 1775 has been estimated at under $12 million.

Benjamin Franklin, who at seventy was the grandee of the Congress, had no philosophical trouble with what was happening. He had personally printed the paper currency of Pennsylvania, New Jersey, and Delaware between 1729 and 1764 at his Philadelphia shop, had written the 1729 pamphlet A Modest Enquiry into the Nature and Necessity of a Paper Currency, and still believed a land-backed issue could work. In Paris, later in the war, he shrugged off French horror at the depreciation with the observation that the currency was "a wonderful machine. It performs its office when we issue it; it pays and clothes troops, and provides victuals and ammunition." That the paper then melted in the holders' hands he considered a kind of voluntary tax — what a later economist would call seigniorage on the unwilling.

Denominations, designs, and a British counterfeiting operation

Early emissions, printed under contract by Hall and Sellers, used a variety of small woodcut emblems and the Latin mottoes of Franklin's old Philadelphia designs — Depressa Resurgit, Si Recte Facies, Fugio. Denominations began at the one-sixth dollar (the eighth of a Spanish dollar, equal to the Spanish real) and ran through halves, thirds, and whole dollars up to eighty dollars for wholesale settlement. Forty different denominations were issued across the forty emissions — a logistical burden that kept printer Hall running day and night through 1778 and 1779.

The British understood the weakness and went to work. Off the tip of Manhattan, aboard HMS Phoenix anchored in New York harbour in 1776, and later aboard additional vessels moored below Staten Island, printers attached to the occupying army produced counterfeit Continental bills at industrial scale. The New-York Gazette and Weekly Mercury of 14 April 1777 ran an open advertisement offering "PERSONS going into the other Colonies" any quantity of counterfeit Congress-notes "for the price of the PAPER per ream" — a line that survives in the period press and which Congress later quoted as wartime sabotage. How much fake paper circulated is disputed. One detailed estimate (Michener, 1988) argues the British volume, combined with smaller private counterfeiting rings in Long Island and Connecticut, was a material fraction of the outstanding stock by 1778; earlier estimates placed it nearer ten percent. Either way, every genuine Continental in a farmer's pocket by that summer was suspect.

From par to 1000 to 1

Depreciation began quietly — a slight premium for specie on the Philadelphia coffee-house market through 1776, largely indistinguishable from the seasonal discount. It accelerated as emissions multiplied. Congress's own report of 29 June 1779 admitted that "the credit of the paper money has fallen in the proportion of twenty to one". By early 1780 the ratio had doubled again, and by the time Congress passed the devaluation resolution of 18 March 1780, the market had already marked the Continental at roughly fifty to one. The resolution ordered that the outstanding bills be called in at forty Continentals for one new dollar of a proposed replacement issue — an explicit repudiation of about ninety-seven and a half percent of the face value still in public hands.

Source: Bezanson (1951); Bullock (1900); Congressional journals

This curve traces the most thoroughly studied wartime hyperinflation of the eighteenth century. A rational-expectations reconstruction of the Philadelphia merchant quotations (Calomiris, 1988) argued that the depreciation path is best explained by a combination of rising expected issues and falling redemption probability — a reading in which the paper was not simply "over-issued" but also correctly priced as a claim whose backing was evaporating. A different framework (Grubb, 2012) reached a related conclusion: the Continental was a zero-coupon bond on a future state with no credible repayment mechanism, and the market priced the bond accordingly.

| Date | Continental dollars per Spanish silver dollar | Cumulative emissions ($ million face) |

|---|---|---|

| Jan 1776 | 1.00 | 6 |

| Mar 1778 | 2.00 | 38 |

| Sep 1778 | 5.00 | 63 |

| Apr 1779 | 10.00 | 115 |

| Nov 1779 | 38.50 | 241 |

| Mar 1780 | 40.00 (official devaluation) | 241 |

| May 1781 | 225.00 | 241 |

| Dec 1781 | 1000.00 | 241 |

Regional acceptance varied in ways that tracked, roughly, distance from the main theatre of war and the presence of British occupation. Boston merchants were conspicuously more willing to take the bills at a moderate discount through 1778, in part because New England state taxes were demanding them back; Philadelphia, briefly occupied by General Howe from September 1777 to June 1778, saw open British refusal and a correspondingly steeper local discount. A monetary-history treatment framed around the quantity theory (Rolnick and Smith, 1985) shows the log-linear depreciation path breaks cleanly into two regimes — one before and one after the autumn of 1778 — with the later regime driven by the market's realisation that no taxing authority stood behind the paper at all.

Tender Acts, Quakers, and the felony of refusing Continentals

As depreciation worsened, Congress and several state legislatures passed Tender Acts making it a criminal offence to refuse Continental bills at face value. Virginia's was among the harshest: a merchant who demanded specie or who priced goods higher in paper than in silver could be prosecuted, lose the contested goods, and in extreme cases face a felony charge. Pennsylvania Quakers, many of whom refused on principle either to fight or to accept what they called "tender money", were jailed and fined through 1778 and 1779. The effect was perverse. Statutes that criminalised market pricing simply pushed transactions into barter or into Spanish dollars exchanged quietly under merchant counters.

John Witherspoon, the Princeton president and New Jersey delegate, argued the economic case against the Tender Acts on the floor of Congress in early 1780. "No law was ever made in any country for regulating the value of commodities", he said, "which did not defeat its own purpose." His 1786 Essay on Money returned to the theme, noting that "a paper dollar is in itself absolutely good for nothing" and that its value depended wholly on the credit of the issuer. The Continental, by that measure, was pricing the credit of a Congress that could not tax.

Devaluation, Robert Morris, and the pivot to specie

Congress's March 1780 devaluation resolution was less a policy than a bankruptcy proceeding. It invited the states to exchange old bills for new at forty to one, with the new bills to be backed five-sixths by the states and one-sixth by Congress. Few states executed. The new issue, printed but thinly circulated, depreciated in turn. By December 1780 George Washington was writing from Morristown that "a wagon load of money will scarcely purchase a wagon load of provisions". Soldiers of the Pennsylvania Line mutinied on 1 January 1781 over pay that had lost almost all its real value — a crisis defused only by specie payments raised through private subscription and French loans.

Congress's response was to hire a chief executive for the finances. On 20 February 1781 it appointed Robert Morris, the Philadelphia merchant-banker who had personally underwritten much of the war effort, as Superintendent of Finance. Morris, assisted by his namesake Gouverneur Morris at the Finance Office, stopped new Continental issues, funded continuing operations on his personal notes ("Morris notes", which traded at par because the market priced his balance sheet above the Congress's), and on 31 December 1781 secured a charter from Congress for the Bank of North America — the first chartered bank in American history. It opened for business in Philadelphia on 7 January 1782 with a capital of roughly $400,000 in Spanish silver, much of it from a French shipment landed at Boston, and began discounting merchant bills at specie par. The pivot to specie-backed banking was decisive. Within eighteen months Morris was rolling over federal obligations through the Bank rather than the press.

Foreign credit filled the gap the press could no longer fill. The French loans arranged by the Comte de Vergennes and pushed politically by Lafayette totalled roughly eighteen million livres by 1782; the Dutch bankers Van Staphorst and Willink, working through John Adams in Amsterdam, opened a line that would eventually exceed ten million guilders; Spanish subsidies arrived through Havana and New Orleans. Treaty of Paris was signed on 3 September 1783. When the accounts were finally totted up, foreign loans and subsidies had covered a larger share of the war effort than the printing press ever did.

"No state shall emit bills of credit"

Political legacy arrived in Philadelphia four years later. Delegates to the 1787 Constitutional Convention remembered the Continental. Oliver Ellsworth of Connecticut argued that "paper money can in no case be necessary. Give the government credit, and other resources will offer." George Mason of Virginia, no fan of strong central government, agreed specifically on this point. Article I, Section 10 of the finished Constitution forbade any state to "emit bills of credit" or to "make any thing but gold and silver coin a tender in payment of debts" — a clause the Convention inserted with almost no debate, and which the ratifying conventions in nine states cited approvingly as an answer to the wartime paper disaster. You can read the matching federal story in our piece on Alexander Hamilton and the birth of American credit, which picks up in 1790 with Hamilton's Report on Public Credit and the assumption of Continental liabilities at pennies on the dollar.

Hamilton's own calculation was unsentimental. His January 1790 report valued the outstanding Continental bills at a hundred to one — meaning a one-dollar bill in a farmer's pocket would be redeemed for one cent of new federal debt — and even that concession was grudging. The same report funded the revolutionary debt, state and federal, at near par in new six-percent stock, and laid the foundation of a credit-worthy sovereign bond market that the Continental's corpse had made politically possible.

The comparative lens and the American suspicion of paper

The Continental is often bracketed with the French assignats of 1789-1796, and the comparison is genuinely useful. Both were revolutionary paper issued by a legislature that had seized sovereignty but not yet built a fiscal apparatus. Both began as credibly backed — Continentals by future state quotas, assignats by confiscated church land — and both slid from discount to disaster as the backing evaporated. The French ended their paper episode at roughly thirty thousand to one; the Americans ended theirs at a thousand to one and walked away. The chronology is close enough that French revolutionaries in 1789 read American pamphlets on why the assignats would not go the way of the Continental, and wrong enough, on the evidence, that those pamphlets were quoted back at them by 1795.

The deeper legacy was cultural. "Not worth a Continental" appeared in print as early as 1781 and had entered newspaper usage by the mid-1780s as the standard American idiom for worthless paper. It carried forward. When Abraham Lincoln's Treasury issued greenbacks in 1862 to finance the Civil War, opponents invoked the Continental by name. The Specie Resumption Act of 1875 and the actual return to gold redemption on 1 January 1879 — a policy debate that dragged through three presidencies — was argued, in part, as a corrective to the wartime paper experiment. The Supreme Court cases known as the Legal Tender Cases (1871, 1884) cited the framers' paper-money suspicion directly, and the gold clause litigation of 1935 did it again. American constitutional anxiety about fiat money has a founding document, and it is a Continental dollar bill.

For readers who want the twentieth-century extremes, the same dynamics play out at larger scale in the Weimar hyperinflation of 1921-1923 and, more recently, in the Zimbabwe hyperinflation of 2007-2009. The ratios there are larger and the technology faster, but the mechanism is the Continental's: a government that cannot fund its expenditures by tax or real borrowing reaches for the press until the press exhausts its own credibility.

Epilogue: the framers' paper in a museum drawer

A single eighty-dollar Continental bill, engraved with a line of thirteen chain-links and the motto We Are One, sits today in the currency drawer of the Massachusetts Historical Society. The paper is browned. The rag fibre shows in the corner. On the back, in a clerk's hand, someone has written "1781 — $1 specie" and underlined the figure twice. The bill is worth, in specie, about the price of a loaf of bread on the Boston market the week Cornwallis surrendered at Yorktown. The republic that issued it lived long enough to write a constitution that would never let it print one again.

Related

Historical records Learn more about our methodology.