A Breadbasket Becomes a Cautionary Tale

For much of the twentieth century, Rhodesia — and, from 1980, Zimbabwe — was known as the breadbasket of southern Africa. Its commercial farms produced surplus maize, tobacco, wheat, and beef; its mines yielded gold, platinum, and chrome; its currency traded at roughly parity with the US dollar at independence. By November 2008, that same country was printing banknotes denominated in hundreds of trillions, abandoning its own currency, and recording an annualised inflation rate estimated at 89.7 sextillion percent (Hanke and Kwok, 2009). No modern nation has destroyed its money faster.

How a functioning middle-income economy spiralled into the second-worst hyperinflation in recorded history — surpassed only by Hungary in 1946 — is a story of political choice rather than natural disaster. Land reform, war finance, and a central bank governor who believed that printing money could conjure prosperity combined to produce a monetary catastrophe so extreme that the Reserve Bank of Zimbabwe eventually printed a single note worth one hundred trillion Zimbabwe dollars. At the moment of its issue, that note would not buy a loaf of bread.

Independence and the Early Years

When Zimbabwe won independence from white-minority rule in April 1980, Prime Minister Robert Mugabe inherited an economy that was diversified, industrial by African standards, and heavily reliant on a small class of roughly 4,500 white commercial farmers who controlled about 70 percent of the most productive land. The first decade of independence saw real GDP grow at around 4 percent a year, education and health spending expanded dramatically, and life expectancy climbed into the low sixties. Foreign reserves were adequate, the budget was disciplined, and inflation stayed in the low teens.

Cracks began to show in the 1990s. An IMF-backed Economic Structural Adjustment Programme from 1991 cut tariffs and subsidies but failed to generate the promised growth, while a severe drought in 1992 hammered agriculture. By 1997, when the government agreed under pressure from war veterans to pay each of them a Z$50,000 gratuity plus a monthly pension — an unbudgeted commitment worth roughly 3 percent of GDP — the fiscal foundations began to crack in earnest. On 14 November 1997, a day Zimbabweans still call Black Friday, the Zimbabwe dollar lost 72 percent of its value against the US dollar in four hours of panicked trading.

Two Catalysts: Congo and the Farms

Two decisions taken between 1998 and 2000 turned fiscal strain into unavoidable collapse. In August 1998, Zimbabwe sent troops to fight alongside Laurent Kabila's government in the Second Congo War, a costly intervention that drained hard currency reserves and is estimated to have cost the treasury at least US$200 million a year through 2002. Soldiers had to be paid in foreign exchange; the Reserve Bank did not have any to spare.

Then came the land. In February 2000, a constitutional referendum that would have allowed uncompensated seizure of white-owned farms was unexpectedly rejected by voters. Mugabe responded by backing "fast track" land reform — in practice, organised invasions of commercial farms by self-described war veterans, often accompanied by violence. Within two years, most of the 4,500 large commercial farms had been seized. Agricultural output, which had accounted for roughly 40 percent of exports and employed a quarter of the workforce, collapsed. Maize production fell by more than 60 percent; tobacco exports, the single largest foreign exchange earner, dropped by around 75 percent between 2000 and 2008 (Richardson, 2005). A country that had exported food to its neighbours now depended on the World Food Programme to feed its own people.

With tax revenue evaporating, foreign investment vanishing, and Western donors withdrawing, the government had only one way left to pay its bills: the printing press.

Gideon Gono and the Printing Press

Dr Gideon Gono was appointed governor of the Reserve Bank of Zimbabwe in December 2003. A banker by training and a Mugabe loyalist by conviction, Gono viewed monetary policy as a tool of political survival. Faced with a government that could not pay its soldiers, its civil servants, or its war veterans, he chose to create the money they demanded rather than tell the cabinet that the cupboard was bare. Broad money supply, which had grown by 104 percent in 2003, expanded by 411 percent in 2005, 1,417 percent in 2006, and an almost incomprehensible 81,000 percent in 2007.

Gono's public statements would have been comic if their consequences were not so grave. He announced "monetary targets" that he missed by orders of magnitude within weeks. He launched Operation Sunrise, Operation Sunrise II, and Operation Sunrise III — three successive currency "reforms" whose main effect was to shave zeros off banknotes so that cash registers and accounting software could keep functioning. He blamed speculators, "economic saboteurs", and Western sanctions for price rises that were, in fact, the direct and predictable consequence of the money he was creating. Economists at the University of Zimbabwe who pointed this out were harassed into silence or exile.

The Redenomination Carousel

Between 2006 and 2009, Zimbabwe redenominated its currency three times. Each reset simply rebased the unit of account; none addressed the underlying fiscal deficit that the Reserve Bank was financing. Each reset bought a few months of convenience before the zeros returned.

| Reset | Date | Conversion | Notes |

|---|---|---|---|

| First dollar (ZWD) | 1980 | — | At par with the original Rhodesian dollar |

| Second dollar (ZWN) | August 2006 | 1 new = 1,000 old | "Operation Sunrise" |

| Third dollar (ZWR) | August 2008 | 1 new = 10 billion old | "Operation Sunrise II" |

| Fourth dollar (ZWL) | February 2009 | 1 new = 1 trillion old | "Operation Sunrise III" |

| Multi-currency regime | April 2009 | Zimbabwe dollar demonetised | USD, ZAR, BWP adopted |

Multiply the three conversions together and one gets a factor of 10^25 — ten septillion. A single fourth-dollar note in 2009 represented 10 septillion of the original 2006 currency, which was itself descended from a unit that had been worth roughly one US dollar at independence. The arithmetic is a monument to what fiscal dominance does when a central bank surrenders to it.

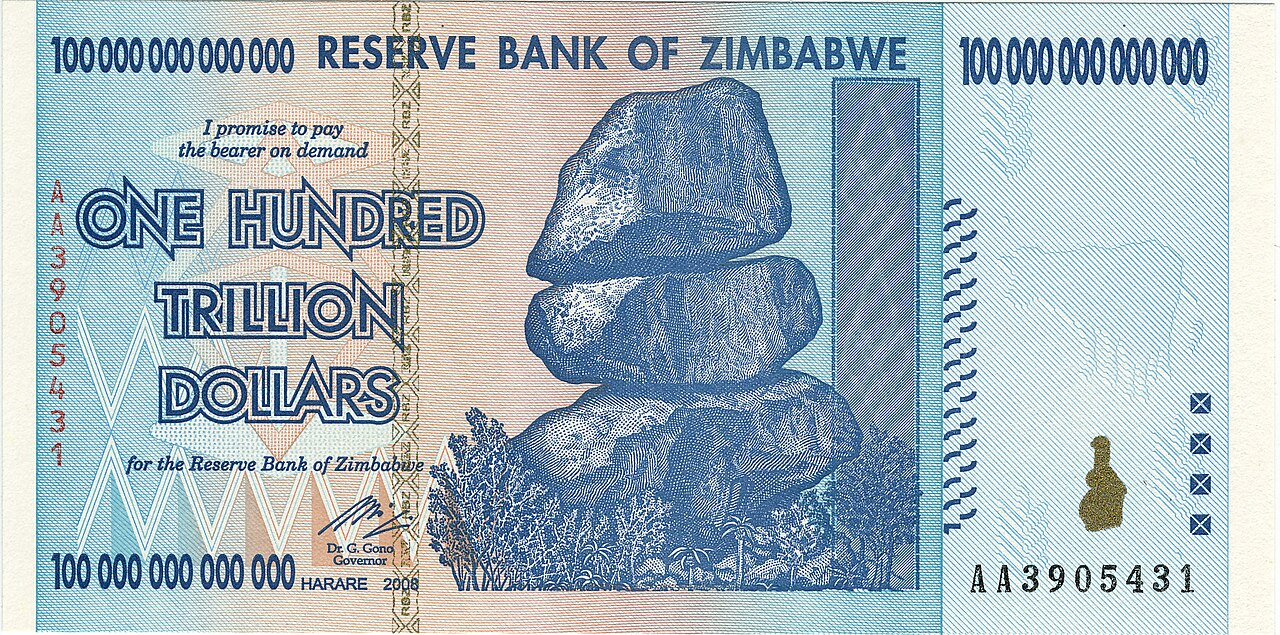

In January 2009, the Reserve Bank issued the final and most famous denomination: a Z$100,000,000,000,000 note — one hundred trillion Zimbabwe dollars. It was the largest-denomination banknote ever legally issued by any government. On the day it was released, it was worth approximately US$30 on the parallel market; within weeks, it was worth nothing at all. Today it sells to collectors on eBay for more than its peak purchasing power ever achieved.

Daily Life at the Edge of the Abyss

Hyperinflation is an abstraction until you live through it. In Harare in 2008, prices were doubling every 24 hours or less. Shoppers carried cash in backpacks, in plastic bags, in wheelbarrows. ATMs were reprogrammed to dispense higher and higher denominations and still could not deliver enough bills for a basic grocery purchase. The Reserve Bank imposed daily cash withdrawal limits which, within a week of being set, were insufficient to buy a single loaf of bread.

Barter returned. Farmers refused to accept Zimbabwe dollars for maize and demanded fuel, fertiliser, or South African rand. Schools that required fees in Zimbabwe dollars found that parents paid in cooking oil or sugar. Doctors asked for payment in US dollars; those who could not pay in hard currency went untreated. Informal dollarisation spread everywhere — by mid-2008, a majority of transactions in urban areas were already being conducted in rand or US dollars long before the government admitted the Zimbabwe dollar was finished. The practice was technically illegal, but enforcement collapsed when even police officers demanded to be bribed in foreign currency.

The social damage ran deeper than the economic. Cholera broke out in August 2008 as water and sanitation infrastructure, starved of spare parts that required hard currency, failed. More than 4,000 people died. Life expectancy, already gutted by the HIV/AIDS epidemic, fell to around 40 for women — among the lowest in the world. An estimated three to four million Zimbabweans, roughly a quarter of the population, left the country, most crossing into South Africa. Remittances sent back by that diaspora became, perversely, one of the main things keeping families at home alive.

Dollarisation and the Death of a Currency

By February 2009, the game was over. The formation of a power-sharing government brought Morgan Tsvangirai of the opposition Movement for Democratic Change into the role of prime minister, and the new finance minister, Tendai Biti, took one decision that changed everything: he stopped pretending. Civil servants were paid in US dollars. Taxes were collected in US dollars. In April 2009, the Zimbabwe dollar was formally suspended as legal tender, and a multi-currency basket — dominated by the US dollar and the South African rand, with the Botswana pula as a third option — replaced it.

Inflation stopped almost immediately. Stripped of its monopoly on a currency it had ruined, the Reserve Bank could no longer finance deficits by decree. Fiscal policy snapped back toward balance because there was literally no way to run a deficit that the central bank could monetise. For the first time in a decade, price tags meant something. The shelves of supermarkets, empty for years, filled again within weeks, now stocked in rand and dollars.

The cost of the cure was the destruction of whatever residual domestic savings existed. Bank accounts denominated in the old Zimbabwe dollar were wiped out; pensions were gone; insurance policies were worthless. A cohort that had lost everything once already lost it again on the transition.

Where Zimbabwe Sits in the Hyperinflation Record

Economists since Phillip Cagan's 1956 paper define hyperinflation as a monthly inflation rate of at least 50 percent — compounded, this means prices more than doubling every two months. By that standard, there have been roughly 57 hyperinflations in recorded history. Zimbabwe's stands out for both magnitude and duration. Hanke and Kwok (2009), who used the parallel exchange rate to back out a daily price index, estimated that in mid-November 2008 prices in Zimbabwe were doubling every 24.7 hours and that the monthly inflation rate reached 79.6 billion percent.

The only episode that was worse was Hungary after the Second World War. In July 1946, prices in Budapest were doubling roughly every 15 hours, and the Hungarian pengő reached a monthly inflation rate of about 4.19 × 10^16 percent before being replaced by the forint. Compared to the classical twentieth-century cases — the Weimar collapse analysed in depth in our Weimar article — Zimbabwe's hyperinflation was both deeper (a much higher peak monthly rate) and longer (running hot for roughly three years rather than Weimar's two). Other comparably severe modern monetary collapses, such as those that followed the Russian GKO crisis of 1998 and the Argentine convertibility collapse of 2001–2002, were severe by any normal metric but belong to a different category altogether; Zimbabwe is not in the same sport.

The Mechanics of Fiscal Dominance

The deep cause of Zimbabwe's disaster was not the printing press. It was the prior decision to run fiscal deficits that nobody would lend to finance. Once a government has destroyed its tax base, exhausted its reserves, and lost access to foreign credit, the central bank becomes the only available lender. Economists call this condition fiscal dominance, and the Cagan model predicts what follows: as real money balances collapse, the government must print ever faster to raise a constant amount of real revenue, until the inflation tax itself stops yielding anything (Sargent, 1982). That is the mathematical logic of a hyperinflationary spiral, and Zimbabwe rode it all the way down.

Three structural conditions made Zimbabwe especially vulnerable. First, the land invasions destroyed the productive base that had generated tax revenue and export earnings. Second, isolation from Western financial markets after 2002 foreclosed borrowing as an alternative to monetisation. Third, the Reserve Bank was an arm of the ruling party rather than an independent institution — Gono answered to Mugabe, not to a monetary policy committee. Any one of these conditions might have been survivable; together they were fatal.

Aftermath: A Country Without a Currency

Zimbabwe spent the decade from 2009 to 2019 without a domestic currency of its own, running what was effectively a US-dollar-based economy. Growth returned — GDP expanded by about 10 percent a year between 2009 and 2012 — but the government had no monetary levers of any kind. It could not depreciate to restore competitiveness, could not act as lender of last resort to its banks, and could not earn seigniorage. As fiscal pressures rebuilt in the mid-2010s, the Reserve Bank began issuing "bond notes" in 2016, officially claimed to trade at parity with the US dollar, unofficially trading at a steep discount almost immediately.

In June 2019, the government re-established a monopoly domestic currency — the RTGS dollar, later rebranded simply as the Zimbabwe dollar — and banned the use of foreign currencies for domestic transactions. Inflation promptly returned: the annual rate exceeded 500 percent in 2020 before stabilising, and has remained high and volatile ever since. In 2024, the government launched yet another new unit, the Zimbabwe Gold (ZiG), ostensibly backed by gold reserves. Faith, however, does not follow from rebranding, and at the time of writing Zimbabweans continue to prefer US dollars for any transaction of significance.

Lessons That Should Not Need Repeating

Zimbabwe proves three propositions that monetary economists have understood for a century but that politicians periodically forget. A central bank cannot remain credible if it is obliged to finance fiscal deficits on demand. A currency cannot outlive the productive base that gives it meaning. And once public confidence in a monetary unit is lost, no rebranding, no new denomination, and no patriotic appeal will restore it — only a credible institutional break with the past, as Hungary demonstrated with the forint in 1946 and Germany with the Rentenmark in November 1923.

The hundred trillion dollar note now sits in the wallets of collectors, a curiosity from a country that briefly held the world record for destroying money. What the note cost — in savings annihilated, lives shortened, and a generation scattered across the region — is the real price of forgetting why central banks exist.

Related

Historical records Learn more about our methodology.